Estimated reading time: 10 minutes

Key Points:

- RSU vesting, bonuses, and raises can feel like a windfall, but they often come with tax implications that require thoughtful planning.

- A strategic approach—prioritizing debt, savings, retirement contributions, and diversification—can turn a one-time boost into lasting financial progress.

- Once your essentials are covered, using part of your windfall to enjoy life can be a meaningful and intentional part of your financial plan.

Table of contents

When a windfall hits your account—whether from a bonus, a raise, or vested RSUs—it often brings a wave of pressure alongside the excitement. Should you celebrate? Invest? Pay something off?

There’s often this unspoken expectation to “do the smart thing.” But what does that even mean when your compensation includes equity, variable income, and layers of tax complexity?

The good news is handling a windfall doesn’t have to mean restriction or hesitation. With a thoughtful, intentional plan, this moment can be an opportunity to build momentum, align your money with what matters most, and move forward with clarity and purpose.

Define Your Windfall

In fields like tech and pharma, compensation packages often extend well beyond base salary. For instance, the National Association of Stock Plan Professionals reports that most public companies now grant RSUs to at least their mid-level employees, making equity an increasingly important part of total compensation.

As a result, windfalls—those larger, sometimes unexpected boosts in income—tend to be more common in these industries. They can take several forms, including RSU vesting, performance bonuses, and significant raises tied to promotions or expanding responsibilities.

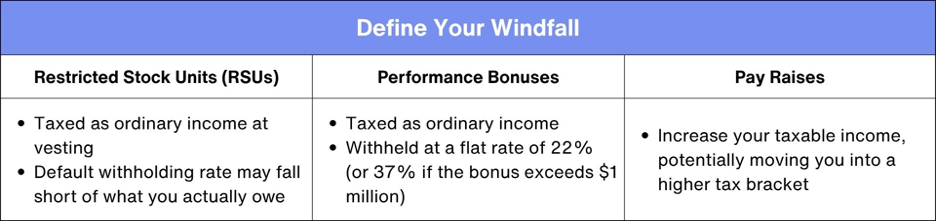

- Restricted Stock Units (RSUs) are a staple in many compensation packages. When they vest, the shares officially become yours, and their value is taxed as ordinary income based on the market price at vesting. This income is typically included in your paycheck, but the default tax withholding may fall short of what you ultimately owe.

- Performance bonuses are also taxed as regular income. However, they’re often withheld at a flat rate of 22% (or 37% if the bonus exceeds $1 million), which can lead to a shortfall at tax time if you’re in a higher bracket.

- Raises tend to feel like an ongoing win, but they increase your taxable income going forward, potentially bumping you into a higher bracket.

While a windfall can feel like sudden financial freedom, it often comes with less obvious tax complexities. Understanding exactly what’s landing in your account—and the tax implications that come with it—is key to making thoughtful, strategic decisions.

Pause Before Spending Your Windfall

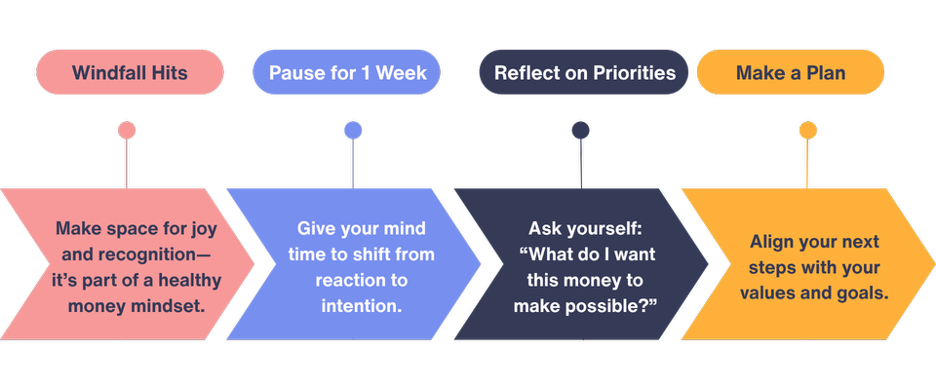

It’s completely normal to want to celebrate when a windfall hits. In fact, allowing space for joy and recognition is an important part of a healthy relationship with money.

That said, big financial moments often come with a surge of emotion—excitement, relief, even pressure to act quickly. Those feelings can lead to impulsive decisions that may not reflect your long-term priorities.

Before making any major purchases or upgrading your lifestyle, pause for at least a week. This brief window of reflection allows you to move out of reaction mode and into intentional planning.

During that time, consider what matters most to you. What do you want this money to make possible—not just today, but in the bigger picture?

Know What’s “Spoken For”

When deciding how to use your windfall, it’s also important to take a step back and look at your overall financial picture. This moment can be an opportunity to either catch up on essentials or get ahead on long-term goals, but only if you know where things stand.

✅ Start by reviewing any high-interest debt. Paying off credit card balances or lingering student loans can provide a guaranteed return by eliminating costly interest charges.

✅ Check in on your emergency fund. If you don’t have at least three to six months’ worth of living expenses saved in an easily accessible account, this may be the time to prioritize it.

✅ Consider any known expenses on the horizon. If expenses like home improvements, tuition payments, or upcoming travel are already on your radar, your windfall may help cover them without disrupting your regular cash flow.

Identifying what’s already “spoken for” can help you gain clarity on how much of your windfall is truly available and how to use it most effectively.

Use Your Windfall to Accelerate Your Financial Goals

Once you’ve addressed any immediate financial priorities, a windfall can be a powerful tool for building momentum toward your longer-term goals. With a thoughtful approach, you can use this opportunity to strengthen your financial foundation, reduce risk, and create greater flexibility for the future.

Here’s a smart, strategic order of operations to guide how you allocate your funds:

- Sell vested RSUs and diversify your portfolio.

- Fund short- to mid-term goals.

- Max out retirement accounts with an employer match.

- Contribute to other tax-advantaged accounts.

- Invest in a taxable brokerage account.

- Treat yourself or others—with intention.

Each of these steps plays a role in turning a one-time income boost into lasting financial progress. Let’s break them down in more detail.

#1: Sell Vested RSUs and Diversify Your Portfolio

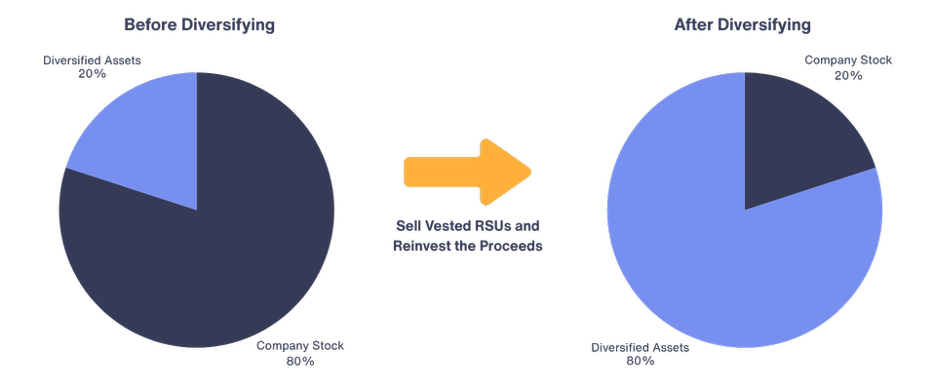

If a significant portion of your net worth is tied up in your company’s stock, you’re likely exposed to what’s known as concentration risk, the financial vulnerability that comes from relying too heavily on a single asset. While it’s common to feel a sense of loyalty or confidence in your employer’s future, home stock syndrome can leave you overexposed if the stock underperforms.

If your windfall comes from vested RSUs, selling those shares and reinvesting the proceeds can be a smart way to reduce concentration risk. Working with an experienced financial professional can help you diversify thoughtfully and efficiently, allowing you to protect your wealth while making the most of your equity compensation.

#2: Fund Short- to Mid-Term Goals

When allocating a windfall, consider what’s on the horizon in the next one to five years. Perhaps you’re thinking of buying a home, planning a wedding, taking an extended trip, or stepping away from work for a career pivot or sabbatical.

These are meaningful life moments that often come with a big price tag. By earmarking a portion of your funds for these goals, you can potentially avoid dipping into long-term investments or retirement accounts, which can trigger taxes, penalties, or interrupt your progress toward financial independence.

#3: Max Out Retirement Accounts with an Employer Match

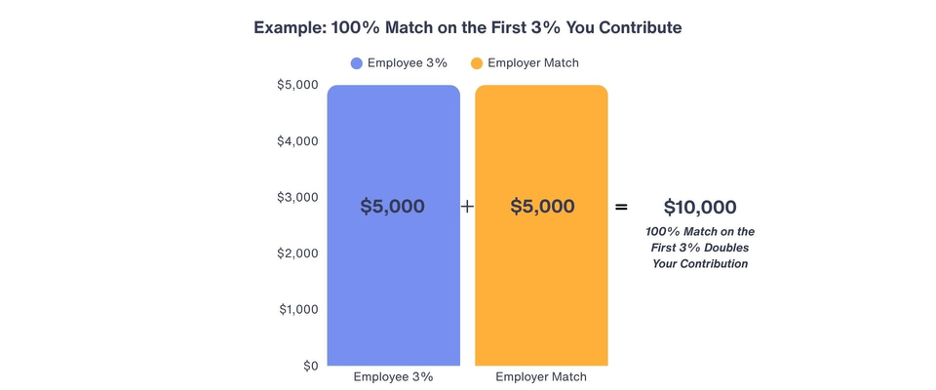

If your employer offers a 401(k) match, contributing enough to earn the full match is one of the most effective ways to accelerate long-term wealth. Missing out on this match can mean leaving a meaningful part of your total compensation package on the table.

Many employers offer to match a percentage of your contributions, typically up to a certain portion of your salary. For example, a common arrangement might be a 100% match on the first 3% you contribute, or 50% on the first 6%.

This match is essentially free money—an immediate return on your investment with no market risk. Over time, these matching contributions (and the growth they generate) can significantly boost your retirement savings.

If your windfall gives you extra cash flow, consider using it to increase your 401(k) contributions for the remainder of the year. This allows you to take full advantage of an employer match without impacting your day-to-day budget.

#4: Contribute to Other Tax-Deferred Accounts

Once you’ve maxed out your workplace retirement plan, look at additional tax-advantaged savings opportunities. For example, contributing to a Traditional or Roth IRA can be an effective way to grow your retirement savings while potentially reducing your tax burden.

In 2025, the annual contribution limit for IRAs is $7,000. If you’re 50 or older, you’re eligible to make an additional $1,000 in catch-up contributions, bringing your total to $8,000.

For those enrolled in a high-deductible health plan, you might also consider contributing to a Health Savings Account (HSA). HSAs offer a unique triple tax advantage: your contributions are tax-deductible, the funds grow tax-free, and withdrawals are tax-free when used for qualified medical expenses.

Whether you use it to cover healthcare expenses now or let the funds grow over time as an additional retirement resource, an HSA can add flexibility and tax efficiency to your financial plan. In 2025, individuals with self-only coverage can contribute up to $4,300 to an HSA, while those with family coverage can contribute up to $8,550. If you’re age 55 or older, you’re eligible to make an additional $1,000 catch-up contribution.

#5: Invest in a Taxable Brokerage Account

Once you’ve maxed out your contributions to tax-advantaged accounts for the year, consider directing any remaining windfall funds into a taxable brokerage account. These accounts offer greater flexibility than retirement accounts—there are no contribution limits, required holding periods, or early withdrawal penalties—making them ideal for building wealth while maintaining access to your money.

Whether you’re saving for a major purchase, funding a future life transition, or simply growing your wealth, this type of account gives you the freedom to invest on your own terms. It also provides opportunities for smart tax management through strategies like tax-loss harvesting and capital gains planning, helping you optimize returns while keeping your tax liability in check.

#6: Treat Yourself or Others—with Intention

If you’ve taken care of your financial priorities and still have money left over, it’s more than okay to use part of your windfall to create joy—in fact, it’s a meaningful way to honor your hard work. That joy might come in the form of a long-awaited vacation, a special purchase, a thoughtful gift, or something as simple as a solo spa day or weekend getaway to recharge.

Investing in your well-being is just as important as investing in your future. When you spend intentionally—aligned with your values and what truly matters to you—it turns a moment of success into something deeply satisfying and memorable.

Making the Most of a Windfall

Windfalls like RSU vesting, bonuses, and big raises reflect your talent, dedication, and leadership. It’s important to pause and celebrate the moment. You’ve earned this.

At the same time, how you handle this financial boost can make a lasting difference. With a clear, intentional plan, your windfall can create greater freedom, reduce stress, and move you closer to the life you envision.

If you’re not sure where to start or simply want to be more intentional about your next financial move, Align Financial Solutions is here to help. We specialize in helping women leaders navigate the complexities of RSUs and stock-based compensation, so you can avoid surprise tax bills, simplify your finances, and use your windfall to build a life of freedom and flexibility.

Our goal is to take the stress out of decision-making and help you feel confident about where your money is going and why. Book a 15-minute Align Call to explore how we can help you turn this financial milestone into meaningful, lasting momentum.

Disclosure:

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.