Estimated reading time: 9 minutes

Key Points:

- Behavioral biases like overconfidence, loss aversion, herd mentality, present bias, and confirmation bias can quietly derail even the most successful women’s financial plans by leading to risky choices, procrastination, or missed opportunities.

- Each bias shows up in everyday ways, such as clinging to underperforming investments, overspending today at the expense of tomorrow, or ignoring perspectives that challenge existing beliefs.

- The path forward is to recognize these patterns, reframe your decisions with data and intention, and, when needed, lean on systems or trusted advisors who help keep your financial plan on track.

Table of contents

- Overconfidence Bias: “I’ve Got This Handled”

- Loss Aversion: “I Just Can’t Let This Go”

- Herd Mentality: “Everyone Else Is Doing It”

- Present Bias: “I’ll Worry About That Later”

- Confirmation Bias: “See? I Knew I Was Right”

- Pulling It All Together

- Keeping Your Behavioral Biases in Check: The Empowering Truth

- You May Also Like

Money is never just about numbers. If it were, none of us would overspend, panic when the stock market dips, or procrastinate updating our wills. We’d all calmly run the numbers, make the most rational choice, and move on with our lives.

But money is emotional. It’s tied to our sense of security, our identity, and even our dreams for the future. That’s why financial decisions can be trickier than expected, even for women who are accomplished, ambitious, and successful in so many areas of life.

The truth is, we’re all wired with behavioral biases that can quietly sabotage our best intentions. These aren’t flaws. They’re part of being human. But if you don’t recognize them, they can keep you stuck in patterns that derail your financial goals.

So, let’s break down the most common biases that might be getting in your way, how they show up in everyday life, and how to shift them so your money starts working for you, not against you.

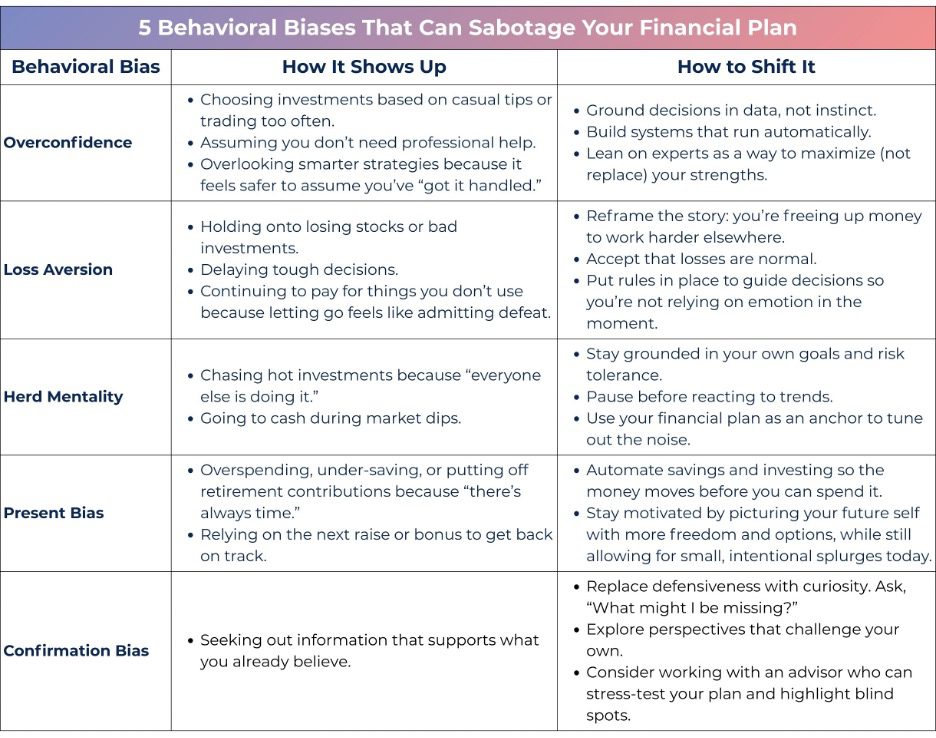

Overconfidence Bias: “I’ve Got This Handled”

Think back to a time you were absolutely sure you could pull something off. Maybe it was running a 10K without much training or cooking a complicated dinner party recipe without testing it first. Sometimes it works out. Other times, not so much.

That same attitude often shows up in money. Overconfidence bias makes us believe we know more than we do, or that we can beat the odds.

For some women, overconfidence shows up as choosing investments based on a casual tip from a friend. For others, it’s the belief that they don’t need guidance with complex areas like taxes or estate planning because they’re “smart enough to figure it out.”

And for many of my clients with equity compensation, it often means holding onto too much company stock because it feels safe, familiar, or like they have an inside edge compared to the average investor.

This behavioral bias can feel deceptively positive. In many areas of life, confidence helps us succeed. But when it comes to money, too much confidence can backfire. It often leads to taking on unnecessary risk, trading more than is wise, or overlooking strategies that could strengthen your plan, all because it feels safer to assume you already have it handled.

How to shift it: Confidence is a strength, but it works best when paired with self-awareness. The most effective way to counter overconfidence bias is to ground your decisions in data rather than instinct. Build systems that don’t depend on you having all the answers, such as a diversified investment strategy that runs automatically in the background.

And remember, leaning on experts isn’t a sign of weakness. It’s a way of making the most of your resources and ensuring your money is working as hard as you are.

Loss Aversion: “I Just Can’t Let This Go”

Suppose you signed up for an expensive gym membership but for one reason or another, you rarely go. Instead of canceling, you keep paying month after month because it feels like giving up would mean you wasted your money. That’s loss aversion at work.

When it comes to money, loss aversion makes us cling to bad investments, hold onto underperforming stocks, or delay tough decisions because the pain of losing feels greater than the pleasure of gaining.

This idea, known as “prospect theory,” was introduced in 1979 by behavioral economists Daniel Kahneman and Amos Tversky, who discovered that people experience losses about twice as intensely as they experience gains. In other words, losing $100 hurts far more than winning $100 feels good.

This imbalance often drives our financial choices. Even if your portfolio would do better by selling the losing stock and moving on, it’s tempting to hold on just to avoid admitting defeat.

How to shift it: Start by reframing the story you tell yourself. Instead of “I’m losing money if I sell this stock,” try: “I’m freeing up my money to work harder elsewhere.”

Losses are a normal part of investing, and even the most successful portfolios include them. What matters is the bigger picture and the direction you’re headed, not any single moment in time.

To keep emotions from taking over, consider setting up rules or systems that adjust your investments for you on a regular schedule, so smart choices happen automatically without you having to second-guess every move.

Herd Mentality: “Everyone Else Is Doing It”

Think about times when everyone you knew was downloading the same new app or rushing to book the same trendy vacation spot. Or maybe friends were all talking about buying into bitcoin when it was making headlines.

That’s herd mentality. We’re social creatures, and if people we respect are doing something, it feels safer to follow along.

In personal finance, herd mentality often looks like chasing the “hot” investment of the moment or pulling money out in a panic when markets dip. History is full of examples, like the dot-com bubble of the late 1990s, or the housing bubble of the mid-2000s that ended in the 2008 financial crisis.

The irony is that following the crowd often means buying at the most expensive point and selling when prices are low, the exact opposite of what it takes to build long-term wealth. There’s a reason they’re called bubbles: eventually, they burst.

How to shift it: Start by grounding yourself in your own goals and comfort level with risk. Your money isn’t meant to chase the latest trend. It’s meant to support the life you want.

Before making a big financial move, take a breath and check in with yourself: are you acting on your own plan, or just reacting to what everyone else is doing? Having a financial plan to reference gives you an anchor, helping you tune out the noise and stay focused on what matters most.

Present Bias: “I’ll Worry About That Later”

It’s Friday evening. You’ve had a long week. Do you cook dinner at home or splurge on sushi delivery?

Let’s be honest, most of us go for the sushi. It solves an immediate problem, and in that moment, we’re not thinking about how a little extra spending tonight might add up over time.

That’s present bias: the pull toward instant gratification at the expense of future benefits.

This bias is especially sneaky when it comes to money. It shows up as overspending, under-saving, or putting off retirement contributions because “there’s always time.”

It’s easy to assume that the next bonus, raise, or windfall will get you back on track. But the truth is, time itself is your most valuable resource for building wealth.

Every year you delay saving or investing, you lose the compounding power that only consistent action can deliver. Even the biggest paycheck can’t buy back lost time.

How to shift it: One of the best ways to outsmart present bias is to take willpower out of the equation. Automate your future by setting up regular transfers into savings and retirement accounts, so the money moves before you even have a chance to spend it. Then, keep your motivation strong by picturing your future self, the version of you with more freedom, more options, and less financial stress because you started early.

And remember, it doesn’t have to be all or nothing. Build in small, intentional splurges along the way so you can enjoy life now without losing sight of your bigger goals.

Confirmation Bias: “See? I Knew I Was Right”

Think about a time you searched for something online and only clicked on the results that backed up what you already believed. That’s confirmation bias at work. It feels satisfying to be “right,” but it can also narrow your perspective.

With money, confirmation bias shows up when we look for information that validates our current views and ignore anything that challenges them.

Maybe you’re convinced real estate is the safest bet, so you brush aside the benefits of diversification. Or perhaps you see the stock market as “too risky,” so you zero in on stories of crashes while overlooking decades of steady growth.

The challenge with confirmation bias is that it keeps us stuck inside our own blind spots. By filtering out what doesn’t match our beliefs, we risk missing valuable insights and opportunities that could strengthen our financial future.

How to shift it: The easiest way to break free from confirmation bias is to trade defensiveness for curiosity. Instead of looking for evidence that proves you right, pause and ask yourself, “What might I be missing?” That simple shift opens the door to new information and better choices. From there, make a point of exploring perspectives that challenge your assumptions.

A trusted advisor can be especially valuable in this process, helping to stress-test your plan and highlight blind spots you might not see on your own. The goal isn’t about proving yourself right. It’s about giving yourself the best possible chance at making strong, informed decisions for your future.

Pulling It All Together

These behavioral biases are part of being human. But when left unchecked, they can quietly sabotage your financial progress.

The good news is that once you can name them, you can change them. Here’s a quick-reference guide to the patterns we’ve covered:

Keeping Your Behavioral Biases in Check: The Empowering Truth

Financial success doesn’t come from being perfect or predicting the future. It comes from being consistent, intentional, and open to change. The moment you begin noticing and reshaping your behavioral biases is the moment your financial plan starts working at its highest potential.

Often, the best way to keep these biases in check is to work with a trusted partner who can bring perspective, objectivity, and support. At Align Financial Solutions, our mission is to make money feel less complicated and more empowering, whether that’s lowering your tax bill, streamlining your financial life, or helping you feel confident that you’re making the right decisions for your future.

If you’re ready for guidance that’s clear, supportive, and free of judgment or pressure, we’re here to help. Schedule a 15-minute Align Call today to learn more and get started.