Written by Hazel Secco, CFP®, CDFA®

Key Points:

- Starting in 2026, the OBBBA will change charitable giving tax rules.

- These changes could reduce the tax benefits of your donations, creating a limited window in 2025 to be strategic and maximize both your charitable impact and tax savings.

- Potential strategies to consider before year-end include giving sooner, bunching donations, making non-cash gifts while they still qualify, using QCDs if you’re 70½ or older, and contributing to a donor-advised fund.

Table of contents

Last month, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law, a sweeping, nearly 900-page tax and spending package. If you haven’t had the time (or desire) to read through it, you’re not alone.

Even so, there are a few important changes worth your attention, especially if you’re a high earner, live in a high-tax state, or include charitable giving in your financial plan. This last piece is particularly timely, since permanent rule changes take effect in 2026 that could reduce the tax benefits you receive from your donations.

That means there’s a limited window to be intentional, so your generosity makes the biggest possible impact for the causes you love and for your own finances. To save you from digging through all 900 pages of legislation, here’s a simple breakdown of the key charitable giving changes and how you can get ahead of them.

Charitable Giving in 2026: New Rules Under the OBBBA

Starting in 2026, the OBBBA will change the way charitable donations are treated for tax purposes. Here’s what’s coming and what it could mean for you:

A New Deduction for Non-Itemizers

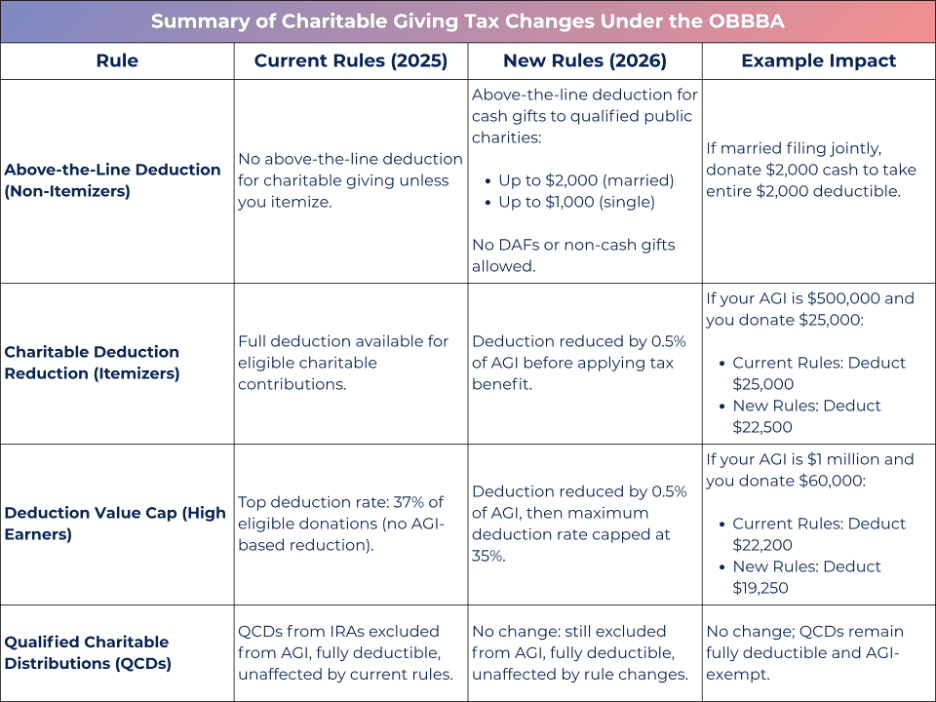

If you typically take the standard deduction (meaning you don’t itemize), there’s good news. Starting in 2026, you can still get a tax break for your charitable giving. Non-itemizers will be able to deduct a portion of their cash gifts to qualified public charities:

- Up to $2,000 if you’re married filing jointly

- Up to $1,000 if you’re single

Just keep in mind, this deduction applies only to cash donations made directly to eligible charities. Gifts to donor-advised funds (DAFs) or non-cash contributions like appreciated stock or household items won’t qualify under this new rule.

A Slight Decrease in Benefits for Itemizers

If you itemize your deductions, which is common if you own a home, have significant medical expenses, or give generously each year, you’ll see a small but permanent cut to the portion of your charitable giving that qualifies for a tax deduction. Starting in 2026, 0.5% of your adjusted gross income (AGI) will be shaved off your eligible donation amount.

For example, if your AGI is $500,000, 0.5% equals $2,500. If you donate $25,000:

- Current rules: You can generally deduct the full $25,000.

- New rules (beginning in 2026): You can only deduct up to $22,500 after the AGI reduction.

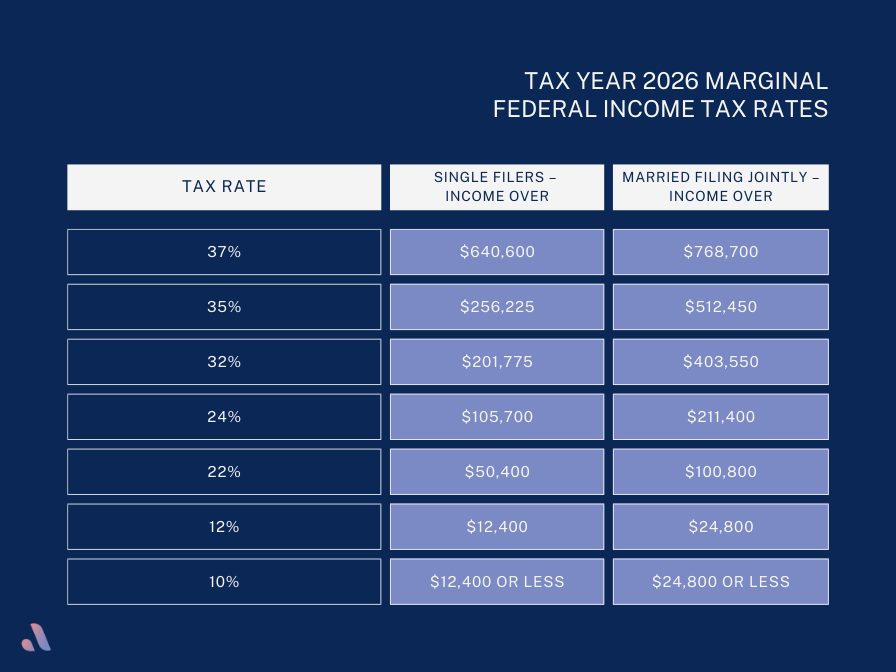

2026 Marginal Federal Income Tax Rates Table

A Bigger Impact for High Earners

If you’re in the top tax bracket, charitable deductions will take a double hit starting in 2026. First, you’ll face the same 0.5% AGI reduction as other itemizers. On top of that, the maximum deduction rate will drop from 37% to 35%.

For example, if your AGI is $1 million and you donate $60,000:

- Current rules: You can deduct the full $60,000 at 37%, saving $22,200 in taxes.

- New rules (beginning in 2026): You first lose $5,000 (0.5% of AGI), leaving $55,000 eligible for deduction. At the new 35% rate, your tax savings drop to $19,250, a $2,950 difference.

What Charitable Giving Rules Are Staying the Same Under the OBBBA

Qualified charitable distributions (QCDs) from IRAs are still one of the most tax-savvy ways for retirees to give, and that’s not changing. QCDs remain fully excluded from your AGI, count toward your required minimum distribution, and keep their full tax benefit under the new rules.

5 Smart Giving Moves to Consider Before 2026

Most of us want to make a difference, and we do. In 2024 alone, Americans gave an incredible $592.50 billion to charity, according to Giving USA.

But here’s the thing: while the heart behind giving is what matters most, how you give can make a big difference too. Without a strategy, you could be missing out on valuable tax benefits that would allow you to give more to the causes you care about.

The OBBBA brings significant changes to charitable giving, but for now, the current (and more favorable) rules are still in place. That means you still have time to be strategic and maximize both your impact and your tax savings.

Here are five ideas worth considering before year-end.

#1: Give Sooner, Not Later

If you know you’ll be making larger charitable gifts in the next few years, it might make sense to give more in 2025. That way, you can take advantage of today’s friendlier tax rules before they change in 2026.

This could be especially helpful if:

- You’re already planning to itemize your deductions this year

- You think your income might drop or your deductions might be smaller in the future

- You’re in a higher tax bracket and want to benefit from the current 37% deduction rate

Not sure if you’ll itemize in 2025? A quick check-in with your financial planner or CPA can help you run the numbers and figure out the best move for your situation.

#2: Bunch Your Charitable Giving to Boost Your Tax Savings Before OBBBA Changes Take Effect

You don’t have to give a huge amount every year to make the most of your deductions. By “bunching” several years’ worth of donations into 2025, you could push your total giving over the standard deduction threshold and unlock bigger tax benefits.

Instead of donating $10,000 in both 2025 and 2026, you could give $20,000 in 2025, itemize your deductions that year, and then take the standard deduction in 2026. You’re giving the same total amount, just in a way that’s more tax-efficient.

For even more flexibility, you could pair this strategy with a donor-advised fund (DAF). With a DAF, you can make the full donation in 2025 to secure the tax break and then distribute the money to charities on your own timeline, whether that’s all at once or over several years.

#3: Give Non-Cash Donations While They Still Qualify

Starting in 2026, the OBBBA’s new rules will mean that non-cash donations (think clothing, household goods, or even appreciated stocks) won’t qualify for the new above-the-line deduction for non-itemizers. In other words, if you plan to take the standard deduction in the future, you won’t get a tax break for these types of gifts unless you itemize.

If you currently itemize but expect to switch to the standard deduction, it’s smart to make any planned non-cash donations in 2025 so you can still deduct their value under today’s rules.

Some examples of non-cash gifts you might consider this year include:

- Gently used clothing or household items

- Vehicles

- Appreciated stocks or other securities

- Collectibles or other tangible personal property

Whatever you give, make sure to keep proper documentation, especially for anything valued over $500, to ensure your deduction holds up at tax time.

#4: Make the Most of QCDs if You’re 70½ or Older

If you’re 70½ or older, qualified charitable distributions (QCDs) remain one of the easiest and most tax-friendly ways to give. In 2025, you can send up to $108,000 (indexed for inflation) directly from your traditional IRA to a qualified charity. That amount can also count toward all or part of your required minimum distribution (RMD) in the same tax year.

Why QCDs are such a win:

- They don’t increase your adjusted gross income (AGI), which can help you avoid higher Medicare premiums and other income-based tax surprises

- They aren’t affected by the OBBBA changes, so they’ll still offer the same tax benefits after 2025

- You can give to more than one charity in a year and still keep your taxes simple

Just keep in mind that the money has to go straight from your IRA custodian to the charity. If you withdraw the money from your IRA first, it’ll count as taxable income and won’t qualify as a QCD.

#5: Use a Donor-Advised Fund to Give Now and Later

A donor-advised fund (DAF) is a great way to make a big, deductible gift now while still spreading your support to charities over time. DAFs can be ideal if you want to bunch donations into 2025 or lock in today’s higher deduction value but still give gradually.

With a DAF, you can:

- Take the full tax deduction in the year you contribute

- Decide when and how to send grants to your favorite charities

- Donate appreciated assets (like company stock) and avoid paying capital gains tax while still getting the full deduction if you itemize

One thing to keep in mind: starting in 2026, DAF contributions won’t count toward the new above-the-line deduction for non-itemizers. So, if you think you’ll take the standard deduction in the future, using a DAF now could be a smart way to make your giving more tax-efficient and sustainable.

The OBBBA & Charitable Giving: Making Your Generosity Count

Giving to charity often comes from the heart, but making your generosity go further takes a bit more strategy. The truth is, these approaches may not be the right fit for everyone, but for the right situations, they can help you maximize both your impact and your tax benefits.

And the good news is they’re not nearly as overwhelming as they might sound. With the right guidance, you can easily weave one or more of these giving strategies into your financial plan before year-end.

At Align Financial Solutions, our mission is to make your money feel less complicated and more empowering, whether that means reducing your tax bill, streamlining your finances, or helping you feel confident you’re making the best choices for your future. If you’re ready for clarity, support, and a plan that’s free from judgment or pressure, we’re here for you. Schedule a 15-minute Align Call and see just how simple financial planning can be.

Disclaimer

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax advice.

We suggest that you discuss your specific tax issues with a qualified tax advisor.