Estimated reading time: 9 minutes

Key Points:

- The Alternative Minimum Tax (AMT) is a parallel tax system that can create unexpected liabilities for women leaders with Incentive Stock Options (ISOs).

- In 2025, higher AMT exemption amounts and phaseout thresholds offer some relief, but women with growing equity compensation remain at risk of triggering AMT, especially in high-tax states.

- Strategic planning can help minimize surprise tax bills and turn equity compensation into lasting wealth.

Table of contents

- The Basics: What Is the AMT?

- ISOs 101: Understanding Incentive Stock Options

- How ISOs Trigger the AMT

- What’s New for 2025: Legislative and Regulatory Updates

- Unique AMT Planning Challenges for Women Leaders with ISOs

- Financial and Tax Planning Strategies

- Your Annual AMT and ISOs Planning Checklist

- Turn Your Equity Into Opportunity

- You May Also Like

For many women in leadership roles, Incentive Stock Options (ISOs) can be a powerful way to build lasting wealth and participate in your company’s success. But they also come with their own set of tax rules, and one of the most misunderstood is the Alternative Minimum Tax (AMT).

In 2025, updates to the tax code make it more important than ever to understand how the AMT works, especially as more women step into executive roles and accumulate meaningful equity. It can get complicated quickly, but once you understand how the AMT interacts with ISOs, you’ll be able to plan ahead—strategically, confidently, and without fear of surprise tax bills.

I know this isn’t anyone’s idea of light reading, so go ahead and grab a cup of coffee (or a glass of wine) before diving in. Let’s break it down in clear, simple terms, and show how a little tax knowledge can go a long way toward safeguarding the wealth you’ve worked hard to build.

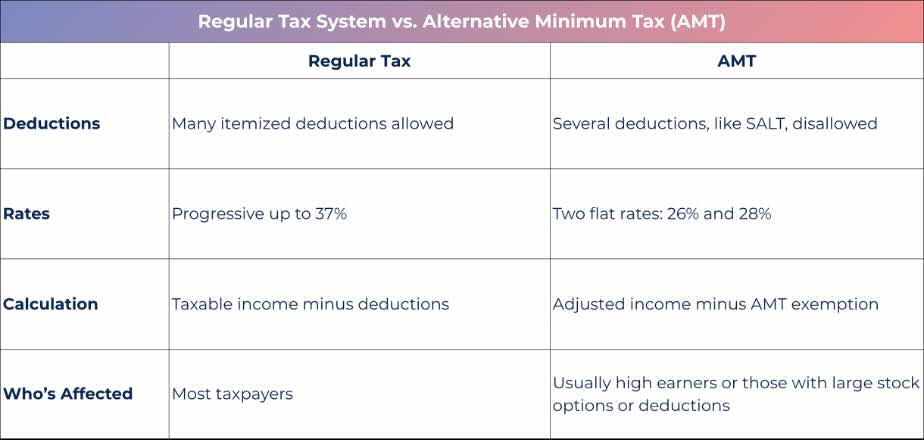

The Basics: What Is the AMT?

The Alternative Minimum Tax is a separate way the IRS calculates your taxes to make sure higher earners pay at least a minimum amount, no matter how many deductions or credits they qualify for under the regular tax system.

Think of it as a parallel set of rules. You calculate your taxes twice: once the regular way, and once under the AMT system. You then pay whichever amount is higher.

The main differences between the two systems come down to what counts as taxable income and which deductions are allowed. Under the AMT, many of the traditional deductions and tax breaks are either limited or completely disallowed. A key example is state and local taxes (SALT), which don’t reduce your AMT income the way they do under the regular system.

Here’s a simple comparison:

ISOs 101: Understanding Incentive Stock Options

Incentive Stock Options are often one of the most significant (and potentially confusing) parts of a compensation package. They give you the right to buy company stock at a fixed “exercise price,” which is typically the value of the stock when the options were granted.

If the company’s value rises over time, you can buy shares at that original lower price and, ideally, sell them later for much more.

Here’s why ISOs are so appealing:

- The potential for long-term capital gains. If you meet the IRS’s holding requirements (at least one year after exercising and two years after the grant date), you can pay the lower capital gains rate (15% or 20%, depending on your income) instead of ordinary income tax when you sell.

- No tax at the time of exercise under the regular tax system, which allows for flexible timing and planning.

This combination makes ISOs an incredible wealth-building tool, especially for women who are increasingly earning equity in leadership and tech roles. However, the tricky part comes when the AMT gets involved.

How ISOs Trigger the AMT

Here’s where things can get complicated, but stay with me. It’s easier to grasp once you understand the sequence.

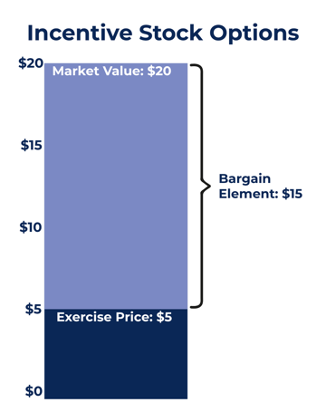

When you exercise an ISO (buying your shares at the set strike price), the IRS looks at the difference between what you paid and what the shares were worth that day. That difference is called the bargain element.

Under regular tax rules, that bargain element doesn’t count as income (yet). But under the AMT system, it does.

Let’s look at an example:

Say you have 10,000 ISOs with an exercise price of $5 per share. When you exercise, the shares are worth $20 each. That’s a $15 “bargain” per share, or $150,000 total.

Even though you haven’t sold your shares or received any cash, the AMT rules treat that $150,000 ($15 bargain element x 10,000 shares) as income for the year you exercised. That can dramatically increase your AMT income and potentially trigger an additional tax bill.

This is why so many people get caught off guard. You can owe tax on paper gains without actually having money in hand to pay it.

What’s New for 2025: Legislative and Regulatory Updates

Tax law changes regularly, but 2025 brings some important updates that affect AMT calculations and ISO planning. Under the One Big Beautiful Bill Act (OBBBA), the AMT exemptions were raised and certain provisions extended:

- AMT exemption amounts for 2025: $88,100 (single) and $137,000 (married filing jointly)

- Exemption phaseout thresholds: $626,350 (single) and $1,252,700 (married filing jointly)

- SALT (state and local tax) deduction cap increased under regular tax but is still disallowed under AMT

What this means in simple terms: higher exemptions make it less likely you’ll fall into AMT territory if your income is moderate. However, once your alternative income (including ISO bargain elements) crosses these thresholds, the AMT can kick in fast.

If you live in a high-tax state like California, New York, or New Jersey, you’re more likely to be affected since the AMT disallows SALT deductions entirely. That’s one reason so many executives in those states find themselves unexpectedly paying AMT after exercising options.

Unique AMT Planning Challenges for Women Leaders with ISOs

As more women step into leadership roles, particularly in industries like tech, biotech, and finance, equity compensation has become an increasingly important part of the wealth equation. Between 2023 and 2024, the share of companies offering stock options to executives rose from 74% to 78%, and for non-executives, from 75% to 77%—a trend that continues to grow as more organizations use equity to attract and retain top talent.

It’s exciting to see more women building wealth through ownership, not just income. But with that opportunity comes complexity, especially when it comes to understanding how stock options interact with the Alternative Minimum Tax (AMT). Greater access to equity often means greater exposure to potential AMT surprises if you don’t plan ahead.

A few factors can make this even more complicated:

- Career transitions. Taking a sabbatical, going part-time, or switching companies can change your income pattern, which affects when and how much you should exercise.

- Promotion years. If you advance into a higher role with a big bonus or RSU vest, that extra income can push you into AMT territory if you exercise ISOs in the same year.

- IPOs or liquidity events. Rapid stock appreciation increases your bargain element and therefore your AMT exposure quickly.

Many of my female clients also tend to think more holistically about their financial picture, which can make AMT planning uniquely challenging. Balancing cash flow, family needs, and long-term goals often requires more nuanced timing and coordination.

Financial and Tax Planning Strategies

Here are some practical ways to approach ISO exercises confidently and strategically:

- Spread out your exercises. Instead of exercising all your ISOs in one year, consider spreading them over several years to stay below the AMT threshold.

- Exercise early in the year. This gives you flexibility. If the stock price drops later, you can sell the shares in the same year and potentially avoid or reduce your AMT bill.

- Exercise when the spread is small. The smaller the difference between your exercise price and the current market price, the smaller your AMT adjustment.

- Understand qualified vs. disqualified dispositions. If you sell shares within a year of exercising, it’s a “disqualified disposition.” This means you lose the long-term capital gains rate but might avoid AMT. If you hold for the required period, you keep the favorable tax rate but risk more AMT exposure.

- Use AMT credits to your advantage. When you pay AMT one year, you may be able to claim a credit in future years when your regular tax exceeds your AMT. It’s not immediate relief, but it can help recoup some of the cost over time.

- Watch your total income in big years. If you also have RSUs vesting, a bonus, or other income spikes, that combination can push you over the AMT threshold. It’s a good idea to coordinate timing with your financial planner or tax advisor.

- Plan around phaseout thresholds. The AMT exemption starts to phase out once your income exceeds the limits. If possible, plan your ISO exercises and other income to stay below them.

- Be strategic about charitable giving. Charitable donations can still reduce your AMT income, but they may be less effective if you’re already deep into AMT territory. If possible, bunch your giving into non-AMT years for better tax impact.

Your Annual AMT and ISOs Planning Checklist

If you hold ISOs, make this checklist part of your annual financial review:

- Review your ISO grant details, including exercise price, vesting schedule, and expiration dates.

- Estimate your potential bargain element and model the AMT impact.

- Plan exercises in years with lower income or fewer other taxable events.

- Track AMT credits and carryforwards from prior years.

- Revisit your plan after promotions, bonuses, or major life events.

- Coordinate with your CPA or financial planner before year-end to explore different scenarios.

- Stay informed on legislative updates and annual IRS inflation adjustments.

A little preparation goes a long way toward keeping your financial plan on track and avoiding last-minute surprises.

Turn Your Equity Into Opportunity

Understanding the Alternative Minimum Tax might not sound thrilling, but it’s one of the smartest and most empowering financial moves you can make as a woman leader with ISOs. With the right strategy, you can minimize surprises, manage your cash flow intentionally, and keep more of the wealth you’ve worked so hard to build.

Remember, you don’t have to figure this out on your own. At Align Financial Solutions, we specialize in helping women in leadership make informed choices about their equity compensation, manage their wealth efficiently, and avoid costly missteps. If you’re ready to take control of your financial future and feel confident about your next steps, schedule a 15-minute Align Call. We’re here to help you turn your equity into opportunity.